Your Books Are Behind. Here's What That's Actually Costing You — And How to Fix It

The Moment You Realize You're Behind

Most business owners don't discover their reconciliation is behind because they were paying close attention. They discover it because something forced them to look. A vendor questions a payment. A loan officer asks for three months of accurate financials and you realize you can't produce them. Tax season arrives and your accountant comes back with a list of questions about transactions from eight months ago that nobody categorized. That's the typical entry point — not a routine check, but a situation that required clean numbers and revealed you didn't have them.

Here's what I want you to understand: the gap between where your books are and where they should be didn't open overnight, and it didn't open because you're careless. It opened because you were out on a job site until 8 PM finishing a HVAC install, or because your fryer broke down on a Friday and the whole weekend became damage control, or because payroll week hit and every hour went toward making sure your people got paid on time. The administrative side of the business — the reconciliation, the categorization, the monthly close — those things got pushed. And then they got pushed again. And eventually, months passed without anyone going back to close them out.

That's a tough spot to be in, but it's also a fixable one. What matters now is understanding the full scope of the problem — not to create anxiety about it, but to size it correctly so you can approach the fix with the same discipline you apply to every other part of your operation.

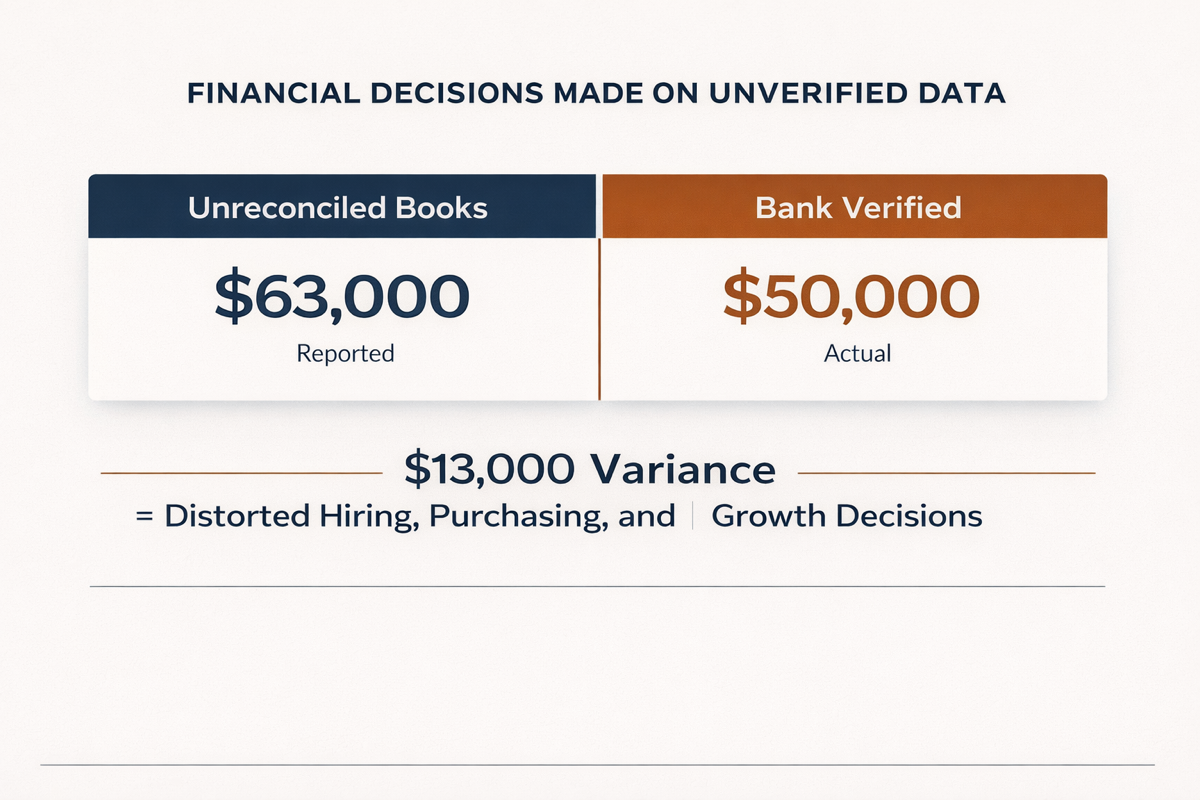

If your bank statement says you have $50,000 and your books say $63,000, you don't have a bookkeeping discrepancy — you have a decision-making crisis. Every hire, every purchase order, every expansion conversation you've had using those numbers has been built on a figure that was never verified.

Unreconciled books aren't a record-keeping issue in isolation. They're a compounding operational problem. The longer the gap stays open, the more financial decisions get made on data that hasn't been confirmed, and the more expensive and time-intensive the correction becomes. Before we talk about how to close that gap, it's worth being clear on exactly what bank reconciliation is and what it's designed to protect against.

What Bank Reconciliation Actually Is (Plain English)

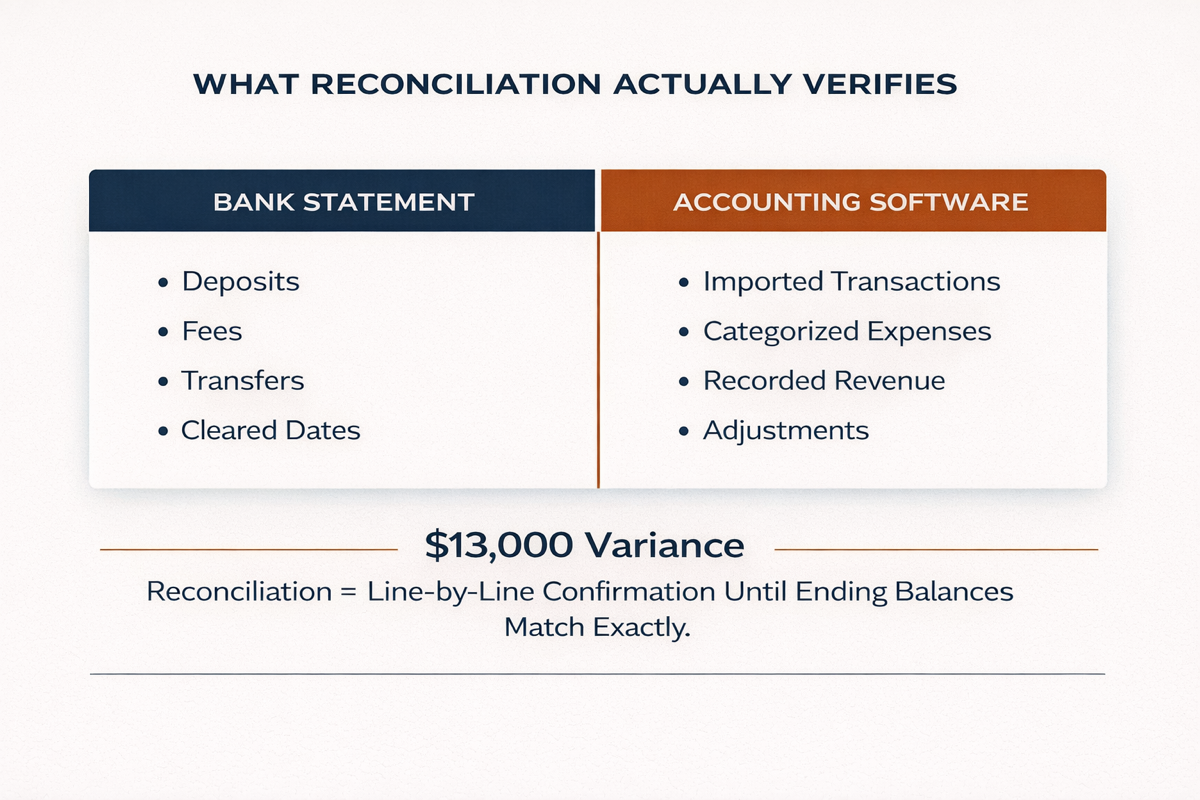

Bank reconciliation is the process of confirming that your business's internal financial records match your actual bank statements — transaction by transaction, account by account, month by month. That's the simple definition. Here's how it works in practice.

Your bank maintains a record of every dollar that moves through your account: every deposit from a customer, every payment to a vendor, every fee, every transfer. Your accounting software — whether that's QuickBooks, Xero, or Zoho Books — maintains its own parallel record based on what gets entered or imported. Once a month, those two records need to be laid side by side and confirmed to match. Any difference between what the bank shows and what your books show is called a discrepancy, and reconciliation is the process of finding those discrepancies, understanding why they exist, and correcting them.

The reason this matters is that your accounting software doesn't automatically know what happened in your bank. It knows what was entered into it. A Square payment that came through on a Tuesday gets imported — but if it got categorized as something it isn't, or if the deposit hit the bank three days later than your books reflect, that creates a difference between your records and reality. A vendor payment that cleared your account but never got logged in your software creates another difference. A bank fee that nobody noticed creates another. Individually, those differences might seem minor. Collectively, across multiple accounts and multiple months, they erode the accuracy of every financial report your business produces.

Your profit and loss statement is only as reliable as the reconciliation process behind it. A P&L built on unreconciled books isn't a financial report — it's an estimate. And running a business on estimates is a different thing entirely than running it on confirmed numbers.

Here's where it gets complicated for a lot of business owners: reconciliation isn't a one-time event. It's a monthly discipline. Every month that passes without it creates a new layer of unverified data sitting inside your books, and that layer interacts with everything that gets entered the following month. Categorization errors from February affect how March looks. Missing transactions from Q1 distort your Q2 cash flow picture. The compounding nature of unreconciled books is why a six-month gap is significantly more than twice the work of a three-month gap — because the errors interact with each other in ways that have to be untangled carefully and in sequence.

What “Catch-Up” Actually Means

When a business owner says they need a reconciliation catch-up, what they're describing is the process of going back through every month in the gap and doing the work that didn't get done — systematically, in order, with the goal of producing a verified and closed set of books for each period. It sounds straightforward. The execution is more involved.

Every month in the gap has to be treated as its own project. That means sourcing the actual bank statements for each account and each month — not just the transaction feed, but the official statements, because those are the authoritative record the reconciliation is verified against. It means reviewing every transaction that was logged in your accounting software during that period and confirming it was categorized correctly, matched to the right account, and recorded at the right date. It means identifying transactions that cleared the bank but were never entered into your books at all. And it means working through the months in chronological order, because you cannot accurately close March until February is confirmed — the beginning balance of each month depends on the verified ending balance of the month before it.

A reconciliation catch-up is not a cleanup. Cleanup implies tidying things that are roughly in order. A catch-up, depending on how far behind the books are, can be closer to a reconstruction — rebuilding the financial record of your business month by month using the bank statements as the source of truth. The distinction matters because it determines the level of expertise, the time investment, and the methodology required to do it correctly.

The scope of a catch-up varies significantly depending on three factors: how many months are in the gap, how many accounts need to be reconciled (operating accounts, savings accounts, credit cards, merchant accounts), and what condition the existing records are in. A business that's three months behind with clean transaction imports and a single checking account is a fundamentally different engagement than a staffing company that's fourteen months behind, has two operating accounts, runs payroll through a separate platform, and has had three different people making entries in the books during that period. Both need catch-up. The approach, timeline, and level of intervention are not the same.

What stays consistent across every catch-up engagement is the objective: to arrive at a state where every month is closed, every account is verified, and the numbers inside your accounting software match the bank statements line by line. That foundation is what makes your financials usable — for tax filing, for loan applications, for cash flow planning, and for the operational decisions you need to make with confidence. Without it, you're working from a set of numbers that looks like financial data but hasn't been confirmed to actually reflect your business.

The Four Industries Where This Shows Up Most

Bank reconciliation problems are not uniformly distributed across business types. They cluster around specific operational patterns — the way cash moves, the platforms involved, and the volume and frequency of transactions. Balanex works primarily across four industries: home services, food service, e-commerce, and staffing. Each one has its own version of the reconciliation problem, and understanding those versions matters because the fix has to match the failure.

Home Services

Consider an HVAC company with twelve technicians in the field. Each tech has a fuel card. Cards are swiped daily across multiple stations, sometimes twice in a day depending on the territory. By the end of the month, there are potentially hundreds of fuel-related transactions across twelve accounts. Now imagine that somewhere early in the year, a banking rule was set up in QuickBooks Online to automatically categorize anything from a gas station as "Fuel & Auto." Efficient, right up until one of those techs uses his company card at a pump that shares a merchant ID with a travel plaza that also sells equipment. The rule fires. The $8,400 equipment purchase gets coded to Fuel. Nobody catches it that month. Nobody catches it the next month either. By Q3, the "Fuel" category is $10,000 over budget, and the owner is trying to figure out whether twelve technicians somehow started filling up tanker trucks — when the actual problem is a single miscategorized transaction sitting undetected inside an automated rule that's been running without human review for eight months.Food Service

The reconciliation challenge for food trucks and food service operators is fundamentally about the gap between what the POS reports and what actually lands in the bank. Square and Toast both generate daily sales summaries. Those summaries reflect gross sales. What hits your bank account is the net deposit after fees, refunds, and payout timing differences — and those two numbers are rarely the same, nor do they always arrive on the same day. A food truck doing $1,800 in sales on a Saturday might see a $1,743 deposit on Monday, $1,809 on Tuesday from the prior Friday's batch, and nothing on Wednesday because of a weekend processing delay. Reconciling those deposits against the POS reports requires matching across different time periods with different net amounts. When that work doesn't happen for four or five months, you end up with a bank account that looks fine and a set of books that's recording the wrong sales figure for the wrong days — and your revenue numbers for the season are quietly distorted.E-Commerce

The reconciliation problem in e-commerce is more subtle and, in some ways, more dangerous because it tends to produce books that look profitable while the business is actually eroding. Shopify and Amazon both pass through merchant fees, fulfillment fees, advertising credits, return deductions, and referral charges before they deposit anything. What arrives in your bank account is already net of those costs. But if your accounting software is recording the gross sale as revenue and not properly accounting for the fee deductions, your revenue looks higher than it is and your expenses look lower than they are. The result is a profit margin that appears healthy — sometimes by several percentage points — when the underlying math on every transaction is negative. A business owner looking at a 12% margin might actually be running at 9%, or breaking even, or losing ground on high-volume SKUs, without any visibility into it until the numbers are reconciled at the transaction level.Staffing

High-volume payroll creates a reconciliation complexity that most generic bookkeeping processes aren't built to handle. In staffing, payroll draws often hit the bank account before the client invoices that fund them are collected. That timing gap — between the outflow and the inflow — creates a cash flow picture that looks like a deficit when it's actually a timing difference. If the books aren't reconciled carefully against both the payroll register and the accounts receivable, those timing differences accumulate. Payroll clears in week one. The client pays in week three. If both aren't being tracked and matched, the business appears to be cash-negative in a way that misrepresents its actual financial position. For a staffing company managing fifteen to twenty clients and bi-weekly payroll cycles, that's a reconciliation that requires precision and frequency — not a once-a-month review.

The Tech Reality: QBO, Xero, and Zoho Books

There's a version of this conversation where I tell you that modern accounting software has made bookkeeping easier, and in some ways that's true. QuickBooks Online, Xero, and Zoho Books are capable platforms. They connect to banks, they import transactions, they generate reports. But capable tools operated without discipline produce capable-looking problems, and there are specific failure patterns inside each of these platforms that show up repeatedly in the books of business owners who thought the software was handling things.

QuickBooks Online and the Banking Rules Trap

QBO's banking rules feature allows you to set up automated categorization logic — if a transaction comes from a certain vendor or contains a certain keyword, automatically categorize it and add it to the books. For high-frequency, low-variance transactions, this creates real efficiency. The problem is that banking rules have no judgment. They apply the same logic to every transaction that meets the criteria, regardless of whether the logic is still appropriate. An HVAC company that sets a rule to categorize all charges from a particular vendor as "Equipment Maintenance" will continue applying that rule even if that vendor later invoices for a $22,000 equipment purchase. The rule fires, the transaction gets added automatically, and it goes into the books as a maintenance expense. That purchase may never get flagged until a CPA asks why maintenance costs tripled in Q4 — by which point the books for three quarters have been produced using the wrong numbers.

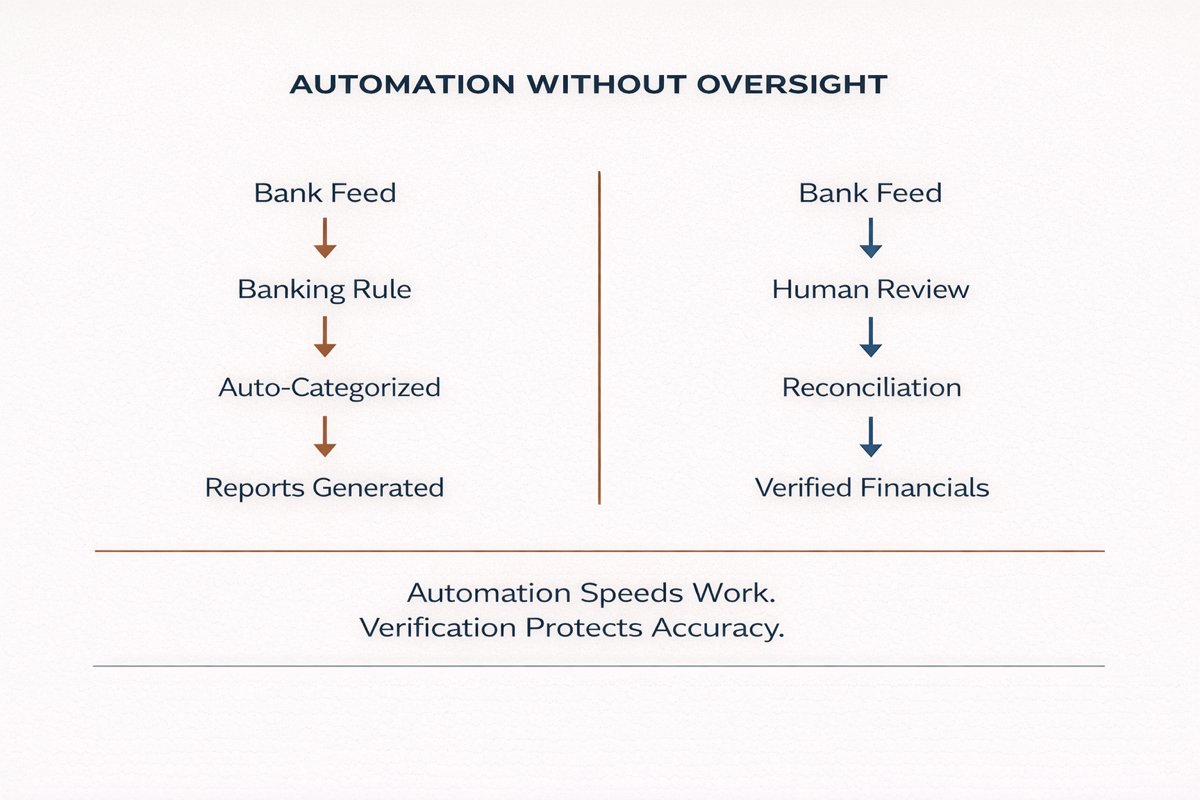

Automation in bookkeeping is a tool for speed, not a substitute for judgment. Banking rules and AI categorization are only as accurate as the human oversight behind them. If nobody is reviewing the output, you aren't automating your bookkeeping — you're automating your errors. And automated errors scale exactly the way automated efficiency does.

Xero and the Reconciliation Hub Illusion

Xero's reconciliation interface is well-designed. It presents unmatched transactions clearly, suggests matches, and marks accounts as reconciled once the balance clears. For users who understand what the process is verifying, it works well. The issue is that clicking through the reconciliation hub confirms that the transactions in your Xero file match the bank feed — it does not verify that those transactions were categorized correctly before they were matched. A transaction can be fully reconciled in Xero and still be sitting in the wrong account, assigned to the wrong category, or attributed to the wrong period. The green checkmark means the balance cleared. It does not mean the balance sheet is right. Those are two different statements, and conflating them is one of the more common sources of books that appear to be reconciled but carry significant categorization errors underneath the surface.

Zoho Books and the Merchant Integration Gap

Zoho Books handles inventory and merchant integrations — Stripe, Square, Shopify — but the reconciliation process between those platforms and the actual bank deposit requires careful attention to how payout batches are structured. Stripe, for example, batches transactions and sends a net payout that may represent two to four days of sales after fees. If Zoho is recording individual sales as they occur but the bank is receiving a single net deposit every few days, the reconciliation between those two data streams requires a matching process that accounts for batch timing and fee deductions. When that matching isn't done correctly, individual sale records sit unmatched in the books, the deposit shows up as unreconciled income, and over several months the cumulative difference between recorded sales and actual deposits grows into a material gap that becomes increasingly difficult to untangle retroactively.

The common thread across all three platforms is this: the software creates the conditions for clean books. It does not produce them automatically. A human being has to be verifying the output on a consistent basis — confirming that what the software categorized and matched actually reflects what happened in the business. Without that layer of human review, every one of these platforms is capable of producing months of clean-looking data that hasn't been verified against reality.

Why Business Owners Let It Slide (No Judgment)

The business owners who find themselves behind on reconciliation are not, by and large, people who don't care about their books. In most cases, they care quite a bit. What they ran out of was time, bandwidth, and — more often than not — a system robust enough to ensure the work was getting done regardless of how demanding the rest of the operation became.

Some had a bookkeeper, part-time or otherwise, who managed it for a while and then stopped — either because they left, because the engagement ended, or because the scope of the work quietly outgrew the arrangement without anyone explicitly acknowledging it. The owner assumed it was still being handled until something surfaced that made it clear it wasn't. Others were managing the reconciliation themselves and doing reasonably well until a growth phase hit — a new crew, a second location, a new client vertical — and the monthly close was one of the things that got deprioritized during the scale. Some simply didn't know it was slipping. They could log into QuickBooks, see transactions importing, see reports generating, and that looked like things were working. The distinction between imported transactions and reconciled, verified books isn't obvious if you haven't been taught to look for it, and most accounting software won't alert you to the difference.

Here's what I want you to understand: intent doesn't fix the books — systems do. Every business owner who fell behind had a reason. Most of those reasons were legitimate. The HVAC owner who was running crews six days a week through peak season wasn't neglecting the books out of carelessness — there weren't enough hours. The food truck operator managing a broken generator and a catering booking in the same weekend wasn't in a position to sit down and reconcile Square deposits. These are real constraints, not excuses. But a legitimate reason for falling behind is not a mechanism for getting current. The reconciliation either happened or it didn't. The gap exists or it doesn't. And the path forward is the same regardless of the circumstances that created it.

The most expensive version of this problem isn't the one where the books are an obvious disaster. It's the one where they look mostly fine. A business that's six months behind on reconciliation but still generating reports has something more dangerous than a visible mess — it has numbers that feel credible enough to make decisions with, but that haven't been verified. That's the environment where significant financial decisions get made with misplaced confidence.

What the catch-up process resolves is not just the backlog. It resolves the uncertainty. It takes a set of books that carries an unknown level of error and converts it into a verified record — one that you can hand to a tax professional, present to a lender, or use as the basis for a business decision without having to mentally discount for the possibility that the numbers aren't accurate. That's the actual value of getting current. Not just compliance. Operational clarity.

The DIY and Automation Trap: A Real Conversation

Earlier this year, a business owner came to us through Balanex LiveHelp℠. She was a several weeks late from her extension tax deadline, her new CPA was waiting on reports, and she needed help getting everything in order. Her expectation, stated plainly in that first session, was that we could look at her QuickBooks file, assist her with getting her books cleaned up, and have her ready to hand off financials within a day.

That's not an unusual expectation. However, It's also not how this works.

When we opened her file, the picture was clear inside of about fifteen minutes. Her banking rules had been running — pulling in transactions, auto-categorizing, marking items as added. From the outside, the file looked active. Reports would generate. Numbers would appear. But nothing had been reconciled. Not January. Not June. Not any month. The rules had been doing work, but reconciliation is not something a rule can perform. A rule categorizes what it sees. Reconciliation verifies that what was categorized is accurate and that every transaction in the software matches what actually cleared the bank. Those two processes are not interchangeable, and one does not substitute for the other.

That was the first conversation. The second one was harder.

When we looked further back, we found that 2023 - 2024 hadn't been reconciled either, including uncategorized bank transactions. Her prior year books — the ones her prior CPA had used to prepare and file her taxes — were built on the same unverified foundation. Rules running, reports generating, reconciliation never completed. She had already filed a return based on those numbers.

The most dangerous numbers in your business aren't the ones you're missing — they're the ones you've already filed with the IRS that were never reconciled. An unreconciled prior year doesn't just create a bookkeeping problem. It creates a tax accuracy problem that you may not discover until an audit surfaces discrepancies between your filed return and what your bank statements actually show.

The conversation we had to have with her was direct but measured. No, we cannot do this in a day. And yes, we need to talk about your 2023 numbers, because if they were produced the same way these are — rules running, no reconciliation — then the return that was filed may not reflect what your bank actually recorded. That's not a bookkeeping issue anymore. That's a tax exposure issue, and it needs to be understood before anyone moves forward.

This is not an unusual story. The specific details vary — sometimes it's a different platform, sometimes it's a part-time bookkeeper who didn't understand reconciliation, sometimes it's a business owner who genuinely believed that connecting the bank feed and setting up rules was the same as maintaining clean books. The underlying structure is the same in most cases: the software was active, the reconciliation never happened, and the problem only became visible when something external — a tax deadline, a loan application, a new accountant asking questions — forced someone to look closely at what was actually in the file.

Rules don't replace reconciliation — they just make the errors harder to find when they inevitably occur. A manual entry that's wrong is visible. A banking rule that's wrong runs silently on every transaction that matches the trigger criteria, potentially for months, and the cumulative effect doesn't show up until you compare what the software recorded against what the bank actually processed.

The Balanex Reconstruction Process

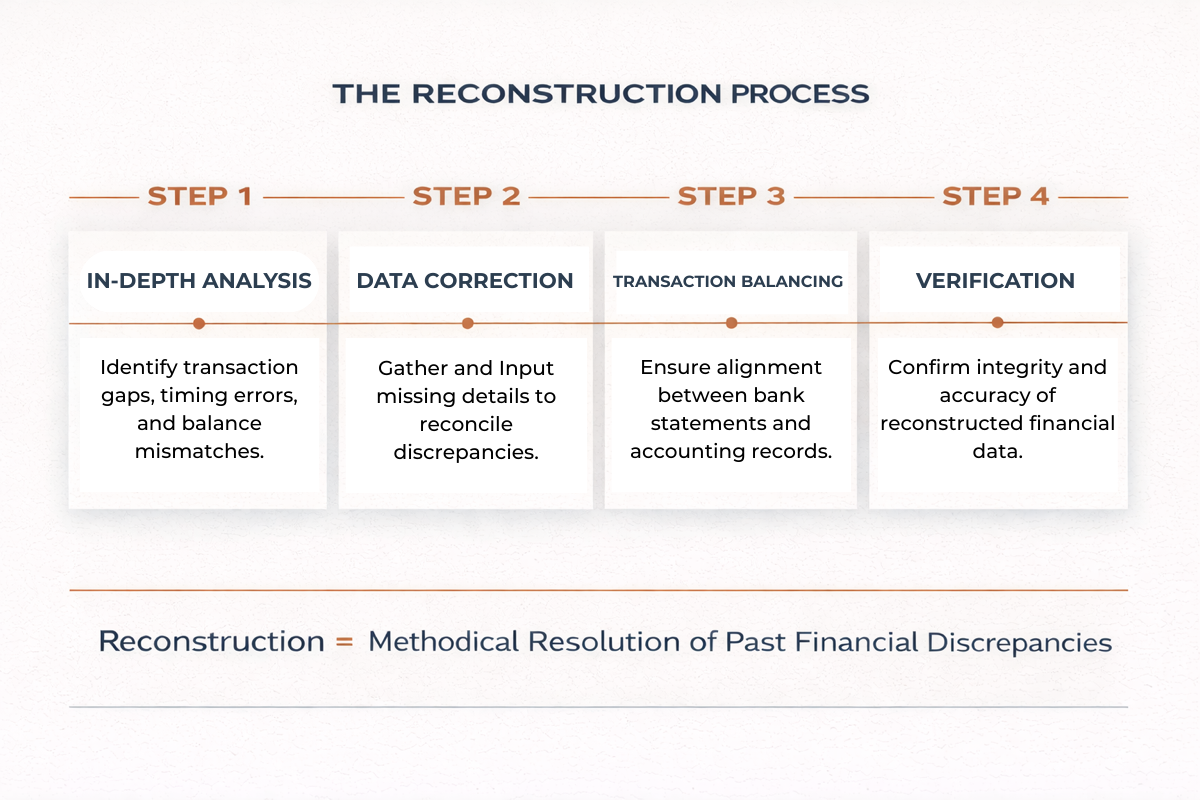

When a client comes to us with the kind of situation described above — multiple unreconciled years, automated rules that have been running unchecked, no verified ending balance to build from — we don't treat it as a cleanup. We treat it as a reconstruction. The distinction matters, because the methodology is different and the sequence of work is not interchangeable.

The first thing we establish before touching anything in the current year is the integrity of the starting point. Every reconciliation depends on a verified beginning balance — the confirmed ending balance from the prior period. If that number is wrong, everything that follows it is built on a flawed foundation. It doesn't matter how carefully you reconcile the current year if the balance you started from was never verified. We see this regularly: a business owner gets help with the current year, the books look clean going forward, but the prior year's ending balance was never confirmed, and the discrepancy between what was filed and what the bank actually shows has been quietly carried forward into every subsequent period.

So we start there. We go back to the last period that was cleanly closed and verified — if one exists. If it doesn't, we go back to the beginning and work forward. That process involves pulling the official bank statements for every account in scope for every month in the gap: operating accounts, savings accounts, credit cards, merchant accounts, and any platform that settles funds into the business's bank. The bank statements are the authoritative record. Everything inside the accounting software gets measured against them.

From there, the work proceeds month by month. For each period, we review every transaction recorded in the software and verify it against the corresponding bank statement line. Transactions that were categorized incorrectly get corrected. Transactions that cleared the bank but were never entered into the software get added. Transactions that appear in the software but have no corresponding bank entry — phantom transactions that entered through an errant rule or a manual entry error — get identified and resolved. Each month gets closed only after the ending balance in the software matches the ending balance on the bank statement exactly.

For businesses running across QuickBooks Online, Xero, or Zoho Books, the platform shapes the methodology but not the standard. In QBO, we audit the banking rules individually — reviewing what each rule is doing, what it's been applied to historically, and whether the logic is still accurate before we allow it to continue running. In Xero, we go beyond the reconciliation hub and review the underlying categorization of matched transactions, because a cleared balance in Xero is not evidence that the categorization was correct. In Zoho, we work through the merchant integration layer — reconciling Stripe or Square payout batches against individual sale records to confirm that the net deposits in the bank are accurately reflected in the books at both the revenue and fee level.

The output at the end of a reconstruction engagement is a set of books where every month is closed, every account is verified, and the numbers in the software reflect what actually happened in the business — not what the rules assumed happened, not what was entered without verification, but what the bank statements confirm. That verified foundation is what everything else — tax preparation, loan applications, cash flow planning, business decisions — should be built on.

Timeline and Expectations: The Honest Version

The most common question we get when a business owner first understands the scope of a catch-up or reconstruction engagement is some version of: how fast can you do this? Sometimes it's framed as a specific deadline — they need clean books for a tax filing in three weeks or a loan closing at the end of the month. Sometimes it's just an expression of the discomfort of knowing the problem exists and wanting it resolved quickly.

Here's what I want you to understand: I'd rather give you an accurate timeline now than have you frustrated two weeks from now when the work isn't done. Professional reconciliation catch-up is a forensic process. It is not a fast-forward button. The work has to happen in sequence, it has to be verified at each stage, and the time it takes is determined by the scope of the gap — not by how urgently it needs to be resolved.

That said, the variables that determine timeline are specific and assessable. The first is the number of months in the gap. A three-month catch-up with a single operating account and clean transaction data is a meaningfully different engagement than an eighteen-month catch-up across two bank accounts, three credit cards, and a merchant account that was never reconciled. The second variable is the condition of the existing records. If transactions have been importing cleanly and categories are mostly correct with some exceptions, the verification process moves faster. If the file has multiple users who entered transactions inconsistently, or banking rules that have been miscategorizing at scale, the correction work is more extensive before the reconciliation itself can even begin. The third variable is documentation availability — whether the business has the bank statements on hand or needs to request them, and how far back that request needs to go.

For a catch-up covering six months or less with a single account and reasonably clean records, a professional engagement typically runs one to two weeks. For more complex situations — multiple accounts, longer gaps, prior-year discrepancies that need to be addressed — the honest range is three to six weeks, sometimes longer depending on documentation gaps. When there are prior-year issues that may have affected filed tax returns, a CPA needs to be in the loop before any amended filings are considered, and that coordination adds time to the process.

What gets produced at the end of that process is worth the timeline. A verified set of books — every month closed, every account confirmed — gives you a foundation that you can use going forward without qualification. You don't have to tell your lender "these numbers are roughly right." You don't have to tell your accountant "I think this is accurate but I'm not sure the prior year was clean." You have confirmed financials, and that changes how every subsequent conversation about your business gets conducted. The business owners who come out of a reconstruction engagement don't just have cleaner books. They have a clearer operating picture, and that clarity compounds over time.

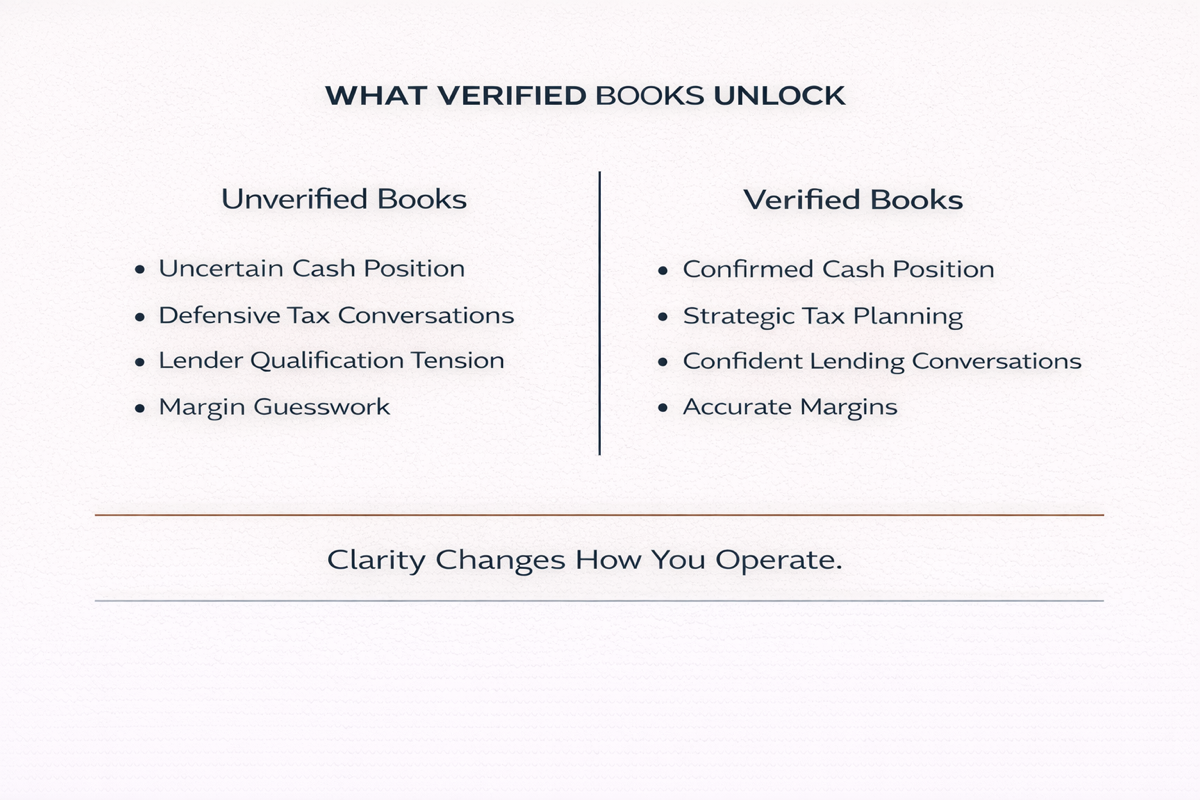

What Clean Books Actually Unlock

There's a meaningful shift that happens when a business owner comes out the other side of a reconciliation catch-up. The work going in is defensive — finding errors, correcting categorizations, verifying balances, closing out months that should have been closed months ago. The work is necessary, but it's reactive. It's fixing what went wrong. What changes on the other side of that process is the ability to move forward without one hand tied behind your back.

Clean, verified books change the nature of every financial conversation you have. When a lender asks for three months of financials, you produce them without qualification. You don't have to caveat with "these are roughly right" or "my bookkeeper has been a little behind." You hand over a set of reports that were produced from reconciled books and let the numbers speak. That distinction matters more than most business owners realize until they've been in a loan conversation where the lender comes back with questions about discrepancies — a month where the P&L doesn't match the bank statement, or an expense category that swings unexpectedly between quarters. Those conversations go differently when the books are verified, because you can answer with specifics instead of uncertainty.

The conversation with your CPA changes too. A significant portion of what tax professionals spend time on during annual tax prep is reconciling the gap between what the client thinks happened financially and what the records actually show. When the books are current and reconciled, that gap doesn't exist. Your CPA spends their time on tax strategy — depreciation schedules, entity structure, timing of income and expenses, deductions that are available but underutilized — rather than on cleanup work that should have been done throughout the year. That's a different quality of professional relationship, and it produces materially better outcomes at tax time.

You cannot scale a home services company or a staffing business on books that haven't been verified. At some point — a second location, a fleet expansion, a major staffing contract — the financial complexity outpaces what unreconciled books can support. Lenders require it. Investors require it. Serious growth requires it. Transparency in your financials isn't a compliance checkbox; it's the infrastructure that makes scaling possible in the first place.

The shift from defense to offense is real, and it's one of the more consistent things we observe in businesses that get their books current and keep them that way. They stop making financial decisions reactively — waiting to see how the month shakes out before deciding whether to make a hire or take on equipment. They start operating from a confirmed picture of where they stand, and that changes the quality of the decisions they make. Not because the numbers became more favorable, but because the numbers became trustworthy.

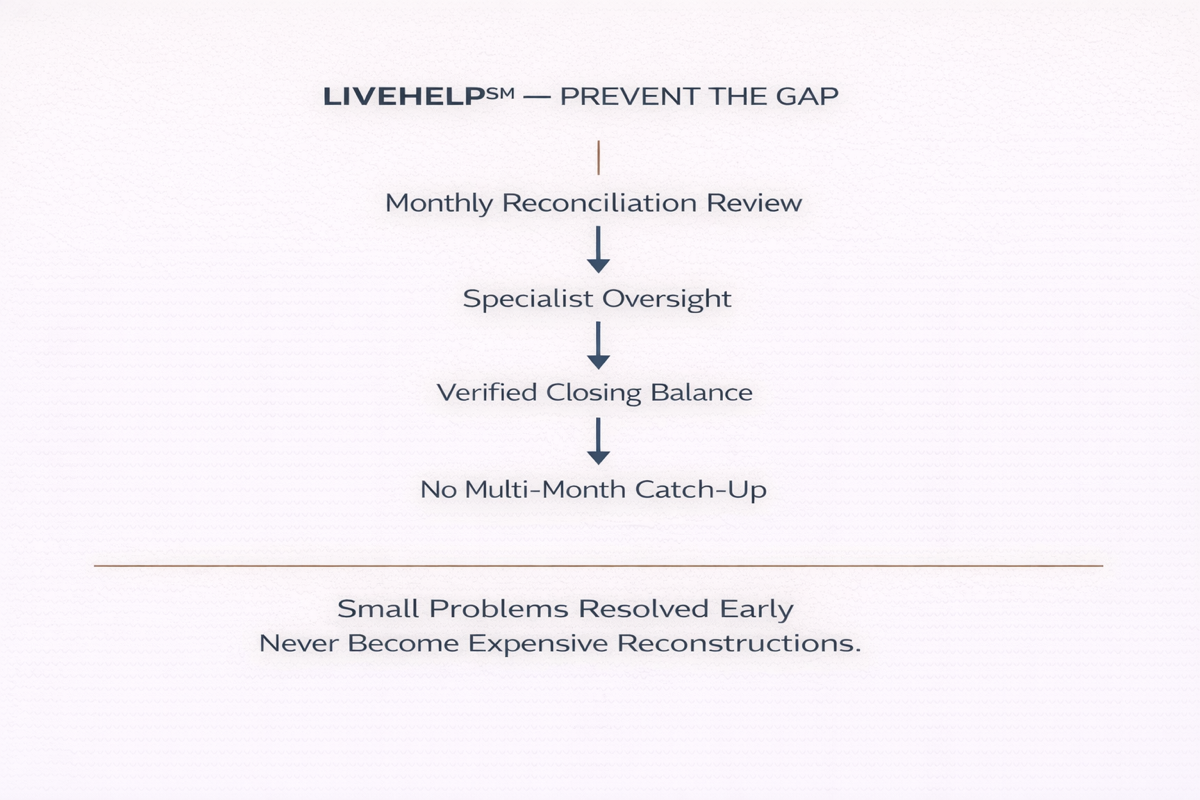

LiveHelp℠: The Bridge for Owners Who Want to Stay Current

Not every business owner who goes through a catch-up is ready to move immediately into full-service bookkeeping. Some have a system they want to maintain themselves. Some are in a growth phase where the economics don't yet support a full-service engagement. Some simply want expert oversight without handing the books off entirely. That's what Balanex LiveHelp℠ is designed for.

LiveHelp℠ is not a chatbot and it's not a knowledge base. It's on-demand access to a Balanex specialist — screen-share support, direct answers to specific bookkeeping questions, and the kind of real-time guidance that prevents the Automation Trap from taking hold in the first place. If you're managing your own books in QBO and you're not sure whether a banking rule you set up six months ago is still categorizing correctly, you get on a LiveHelp℠ session and work through it with someone who can look at the actual file with you. If a Stripe payout came through and the reconciliation doesn't clear, you don't sit with the discrepancy for three weeks — you get it resolved with a specialist who understands how merchant integrations interact with your accounting software.

The value of LiveHelp℠ in the context of reconciliation is specifically this: it keeps small problems from becoming the kind of multi-month catch-up we've been describing throughout this post. The business owner who checks in with a specialist once a month — walking through their reconciliation, flagging anything that looks off, confirming the closing balance — is the business owner who never accumulates a six-month gap. The oversight that prevents the problem from compounding is not difficult to maintain. It just has to be maintained consistently, and LiveHelp℠ is the structure that makes that consistency accessible without the commitment of full-service bookkeeping.

For business owners who came through a catch-up or reconstruction engagement and want to stay current on their own terms, it's the right bridge. Clean books going in, expert guidance to keep them that way.

Closing: The Business Owners Who Get Ahead

Bank reconciliation isn't complicated as a concept. You have a bank statement. You have a set of books. Those two things should match — every transaction, every account, every month. The complexity comes from everything that works against that matching process in a real business: the volume of transactions, the platforms involved, the automation that categorizes without judgment, the months that go by without anyone verifying that what the software recorded is what the bank actually processed.

The business owners who stay on top of this aren't necessarily more sophisticated than the ones who fall behind. They've just built systems — or engaged support — that ensure the verification is happening regardless of how busy the operation gets. They're not reconciling because they love accounting. They're reconciling because they understand that every decision they make about their business — every hire, every equipment purchase, every growth conversation — is only as sound as the numbers it's based on.

The ones we work with know their real cash position at any given time. They know their actual margins, not the estimated ones. When a lender asks for financials, they don't feel the familiar tension of producing reports they're not entirely confident in. When their CPA asks a question about a specific transaction, they can answer it. They operate differently — not because they're better business owners, but because they've removed the uncertainty from their financial picture. And that changes everything about how you plan, how you hire, how you grow, and how you present your business to anyone whose decision depends on your numbers being accurate.

Without that? You're flying blind. And in home services, food service, e-commerce, and staffing — businesses where margins are real and cash timing is unforgiving — flying blind is an expensive way to operate.

Getting current on your reconciliation doesn't just fix the past. It changes how the next month goes. And the month after that. A verified set of books is the foundation that everything else in your business gets built on.

That's what I want for your business.

Balanex provides weekly bookkeeping, full service payroll, and on-demand LiveHelp℠ support for small business owners in home services, food service, e-commerce, and staffing. If your books are behind or you're not confident in what your numbers are telling you, start with a conversation.

Jonathan N.

Author

Jonathan is CEO of Balanex, a financial operations firm that helps small business owners stop flying blind and start making confident decisions with clear numbers. With 27+ years of hands-on experience managing complex bookkeeping, payroll, and financial operations—including managing accounting for Series B startups through IPO and overseeing payroll for 2,500+ employees—Jonathan has worked with hundreds of businesses across home services, food service, e-commerce, and staffing. A QuickBooks ProAdvisor since 1997 and former Intuit Quickbooks Live employee, he specializes in translating financial chaos into actionable strategy.

Disclaimer:

The content on this blog is for informational purposes only and does not constitute financial, tax, legal, or accounting advice. Balanex is a bookkeeping firm — not a CPA, Enrolled Agent, financial advisor, or attorney. Always consult a licensed professional before taking any action. Read our full disclaimer here.